This is a post I’ve been meaning to write, because it’s one I could have used myself, about a year and a half ago. Deciding to give up your US Green Card isn’t an easy decision, but once you’ve made up your mind, the process shouldn’t be so mysterious.

As always, I’m not a lawyer and this in no way constitutes legal advice. I’m documenting my personal experience for purely informational purposes. You should seek qualified legal advice pertaining to your specific situation. That being said, here’s my step-by-step account of how (and a little bit of ‘why’) to formally renounce your US Green Card.

How to Formally Renounce a US Green Card

Firstly, why is this even a thing? And in what scenarios could it apply to you? In this post, I’ll walk you through one way of (ahem) gracefully exiting the US immigration (and, possibly) tax system.

Step 1: Be a Green Card Holder

If you’re reading this, you most likely know what a Green Card is, but let’s recap: what’s commonly referred to as a US Green Card is also known as Lawful Permanent Residency. It’s a legal right to live and work in the US that non-US citizens can obtain if they meet certain conditions. These conditions are usually based on either family or employment.

Unlike a visa (such as H1B, L1, etc), a Green Card is generally renewable, basically indefinitely. It’s typically not quick or easy to become a Green Card holder, but once you are, it’s essentially a done deal. You can do most things (except vote) that a US citizen can do. You need to renew it every 10 years, but that’s about it. While you’re living in the US full time, it’s pretty low-maintenance.

However, when you’re thinking about spending significant chunks of time outside the US, or even moving elsewhere permanently, then things get more interesting, and you have some choices to make.

*Even as someone who went through the Green Card process on relatively ‘easy mode’, I can still attest that it wasn’t easy, quick, or cheap. And I know it’s something many people wish they could attain. I don’t take that privilege lightly. Furthermore, being in a position to voluntarily give up that status is also a privilege, and not one that’s equally open to everyone.

Step 2: Make an Informed Decision

Here, in a nutshell, is how it works: as a Green Card holder, you have two different systems to consider, the immigration system and the tax system. And their rules don’t always align. So, the first step is to be aware of what the immigration implications are, and then you need to understand what tax implications follow from that.

At this stage I hasten to remind you that I’m not an attorney, nor an immigration specialist. However, from my reading, I concluded that absence from the US for extended periods would more or less invalidate my Green Card from an immigration perspective.

Being away for a few months, and especially if there is an intent to return, is quite different to moving away with no plans of returning to the US to live on a permanent basis. For people in the former group, there are pathways they can explore if they wish to maintain their Green Card. For myself, and for others, there was no such intent. I decided that I was comfortable with my decision to give up the Green Card for immigration purposes.

From there, I considered the tax implications. As all Green Card holders should be aware, holding a US Green Card means you are considered a ‘US person’ and therefore a US tax resident, and are subject to tax on your worldwide income, the same as a US citizen is. This is true even if you spend most of your year outside the US (in other words, the Substantial Presence Test, which looks at days of US presence, does not apply to you).

And here’s where it gets interesting. While there are a number of ways for your Green Card to become invalid for immigration purposes, there is only 1 way for it to cease to make you a ‘US person’, subject to US tax on your worldwide income, and that is to follow the process outlined below.

This is why you should be both informed and intentional about this choice. Simply leaving the US and allowing the Green Card to expire can have unwanted tax consequences. And leaving the country for too long, with the hope of just coming back to resume US residence, can have unwanted immigration consequences.

First, decide on your preferred outcome for immigration purposes: Do you want to maintain your US Green Card, and are you willing and able to meet those requirements while you’re (temporarily) outside the US? Or, are you deciding to cease to be a US Green Card holder? If so, you’ll want to make a clean break, and the following steps are for you.

Step 3: Make a Clean Break

So, you’ve decided that you no longer wish to maintain your Green Card for immigration purposes, and you would like your tax status to match. You now have some more decisions to make.

First, when are you planning on leaving? Know that your US residency termination date isn’t always easy to determine. If possible, you’ll want to be aware of your residency termination date, and to plan for it in advance.

Next, you’ll need to be absolutely clear on whether or not the Expatriation Tax rules under IRC 877A apply to you.

Then, and only then, will you want to commence filing the paperwork. Below, I’ll discuss each of these factors separately: residency termination date, expatriation tax under 877A, and filing the appropriate paperwork.

Step 3A: Plan for your (tax) Residency termination Date

When you cease to be a US Green Card holder, via the process outlined here, you may also cease to be a US tax resident. This means you potentially have a choice to make about exactly which day is your last day as a US tax resident.

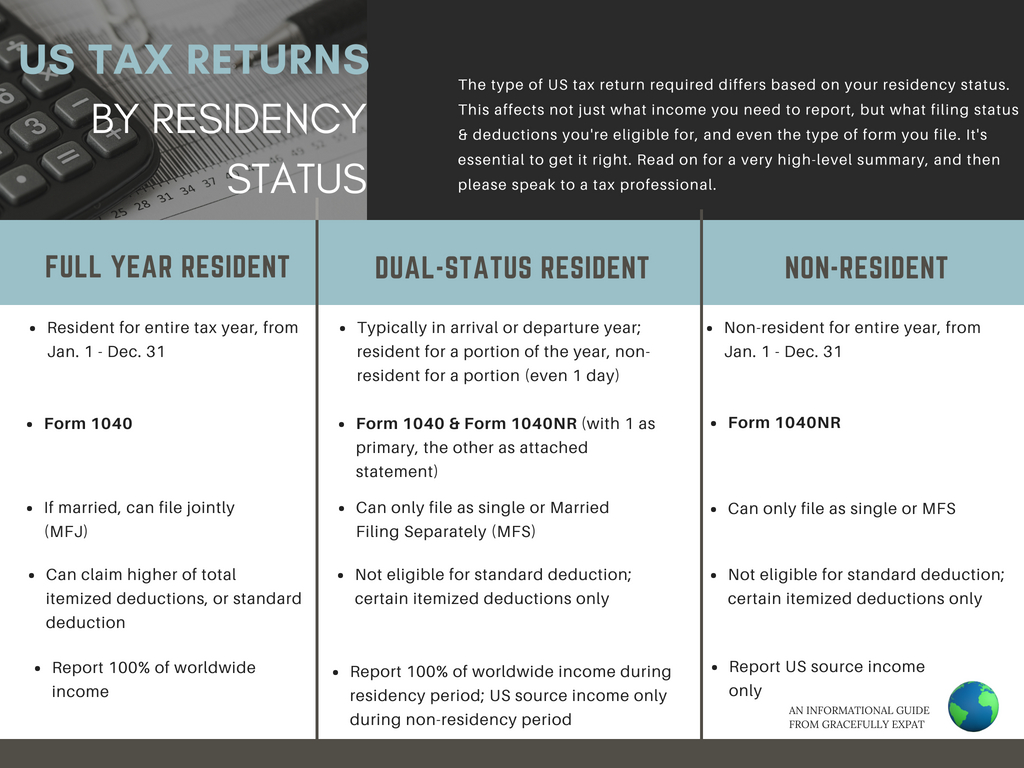

Why does this matter? Well, something that many people don’t consider is that your residency status dictates what kind of tax return you file, and what income you report. Here is a brief, and very simple summary of how to determine your residency termination date for tax purposes. This can’t cover all possible complexities, so please consult a tax professional about your particular situation.

A few general rules to keep in mind:

- Generally, your residency termination date is the later of, the last day you held a US green card, or the last day you were physically present in the US in that year.

- In your departure year, a residency termination date on any day prior to Dec. 31 will result in a dual-status resident tax return.

Your residency termination date is important because it is the date before which, you were taxable/reportable in the US on your worldwide income, and it is the date after which, you are taxed as a non-resident, and subject to US tax only on your US source income. This is a big change.

Furthermore, when you are a full-year US resident, you file a ‘normal’ form 1040, and you are eligible to claim all the ‘normal’ exemptions and deductions, including the standard deduction.

When you are a non-resident all year, you file a form 1040NR, and you aren’t eligible for the standard deduction (this’ll get even more interesting for 2018 1040NR’s, because of the Trump Tax Reform. More on that later).

And when you are a dual-status resident, you file an unwieldy hybrid of the two. You need to file form 1040 for the period in which you were a resident, and form 1040NR for the period in which you were a non-resident. And whichever status you held at the end of the year, is the ‘primary’ form you file, with the other form attached as a statement. It can get messy.

Dual-status residents are also not eligible for the standard deduction, not even a prorated portion for the time they were residents, which has always seemed a bit stingy to me. But the tax code is really, really not designed for us country-hopping weirdos.

Oh, and neither non-residents nor dual-status residents can file a joint tax return, if they’re married. You can see how this could throw a lot of people’s yearly tax planning into disarray, especially because these facts aren’t well known.

Here’s a very high-level summary of the differences in filing statuses, based on residency.

So, how can you, the prospective future former Green Card holder, plan for your residency termination date, and therefore the type of departure year tax return you’ll file?

Here’s what I did as one possible example to get you thinking, but first a caution:

There are simply too many permutations to discuss them all, and their potential consequences, here. If you’ve any doubts, potential complexities, or questions about your residency status, or residency termination date, I cannot urge you strongly enough to contact a tax professional before you take action, and before the end of your last year in the US.

This is one area where it’s just not possible to change the facts after they’ve transpired. If you come to your friendly neighbourhood expat tax pro in March, after you’ve moved outside the US and filed your paperwork the prior October, she’ll be able to tell you what your status is, but neither she, nor the powers that be, not even Cher, can turn back time.

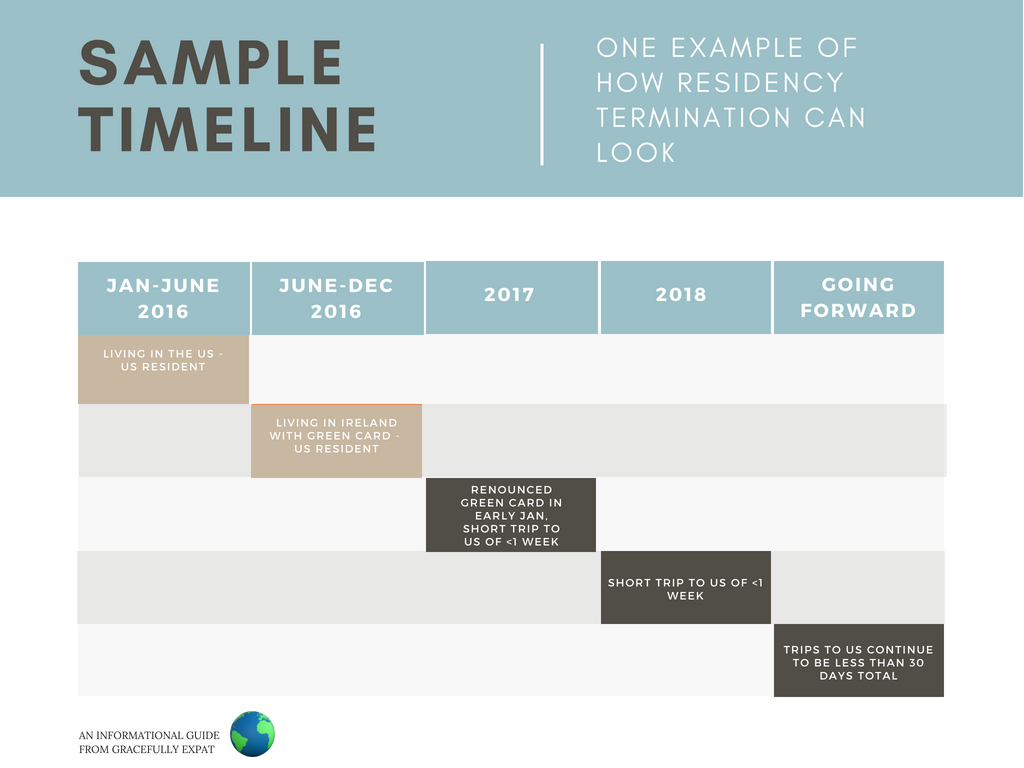

So what did I do? After having lived in the US with my Green Card for 8 years, I moved to Ireland in June 2016. I was pretty sure I wasn’t going to try to preserve my Green Card, because I was pretty sure I’d be moving outside the US permanently. But I gave myself a little breathing room. I decided I wouldn’t decide, until the end of the year.

Then, in early January 2017, I filed my paperwork to formally renounce my Green Card, on the basis of having moved permanently outside the US.

And what was the result of this fact pattern?

Because I was a Green Card holder for all of 2016, I filed a full-year resident tax return for 2016, reporting my worldwide income, including what I’d earned in Ireland, and claiming a foreign tax credit for the Irish taxes I’d paid.

Then, in 2017, I had two tests to look at:

- the Green Card test, which states you’re a resident for any days in which you held a Green Card, and

- the Substantial Presence Test (SPT), which looks at how many days you’ve been physically present in the US in the current year, plus the last 2 years. (Crucially, one requirement of the SPT is that you be physically present in the US for at least 31 days in the current year.)

In 2017, I held a Green Card for 3 days, as I mailed in my paperwork on Jan. 3. Then I spent only about a week back in the US for a family wedding in May. Therefore, I was a non-resident in 2017.

If I’d filed the paperwork later in 2017, not that much would’ve changed, except that I’d have been a dual-status resident on my 2017 return. However, if after filing my paperwork, I’d have had to spend significant amounts of time back in the US, that could’ve seriously complicated things, by potentially pushing my residency termination date back to the date of my last trip.

This is why your tax professional needs to know your complete fact pattern to advise you on this. It’s just too important not to get it right.

So, to summarise, all Green Card holders need to figure out what their residency termination date will be, and all former Green Card holders will file either a form 1040NR (non-resident) or a dual-status resident return in the year they renounce their Green Card.

This next bit will apply, in varying degrees, to only some former Green Card holders, but it’s still important for everyone to understand.

Step 3B: Understand how IRC. 877A (Exit TAx) applies to you

Ah, the joys of IRC. 877A. It’s a section of the tax code worthy of a much more in-depth treatment than I’m going to provide here. My goal is simply to make you aware of it, and to offer you some very rough guidelines as to when you might need to speak to an expat tax professional in detail. If 877A definitely doesn’t apply to you, then it may be enough to cordially acknowledge its existence, and go on about your expatriating in peace.

Often, normal peoples’ brains begin to shut down when we tax geeks start quoting code sections. The reason I like to refer to this one by its code section is to avoid confusion. It’s sometimes referred to as the ‘exit tax’ but that doesn’t quite tell the whole story, as 877A may have requirements of you, even if it doesn’t involve you actually paying any ‘exit tax.’

And talking about ‘expat’ or ‘expatriation tax’ is confusing too, as US citizens and Green Card holders who live and work outside the US are often referred to as ‘expats’, and they pay ordinary tax that has nothing to do with 877A.

So, IRC. 877A it is.

What is it? Well, it’s a potential tax reporting requirement for people ceasing to be US persons, by virtue of giving up their US citizenship or renouncing their US Green Cards. It’s required for all former US citizens, and for some former Green Card holders.

Since we’re talking about giving up your Green Card here, let’s focus on the latter group.

The below flowchart gives a high-level guideline to determining if, and how, 877A apples to you.

‘Long-Term’ Green Card Holders Only

First, only ‘long-term’ Green Card holders are subject to 877A. This means holding your Green Card in at least 8 of the last 15 years.

Please note how this is calculated: it’s “in” 8 of the last 15 years. This includes even 1 day in each of those years. So if you got your Green Card in December 2011, and gave it up in January 2018, this applies to you, even though you only had your Green Card for 6 full years and a few weeks.

If you’re getting close to the 8 year mark, and especially if you know the nastier parts of 877A would apply to you, you may wish to consider your long-term plans with regards to your Green Card. This is another of those areas where you can’t turn back time, so a little advance planning really pays off.

If you’re a ‘long-term’ Green Card holder, then you definitely have to do something regarding 877A. Exactly what that is, depends on whether you’re a ‘covered expatriate’ or not. More definitions ahead!

Covered Expatriates

The next thing to determine is, are you a ‘covered expatriate’ or not? This will determine the arduousness of your 877A requirements, and whether or not you may owe any ‘exit tax.’

Here’s how the IRS defines a ‘covered expatriate’:

- Your average annual net income tax for the 5 years ending before the date of expatriation or termination of residency is more than a specified amount that is adjusted for inflation ($160,000 for 2015, $161,000 for 2016, $162,000 for 2017, and we can assume a similar amount for 2018), or

- Your net worth is $2 million or more on the date of your expatriation or termination of residency, or

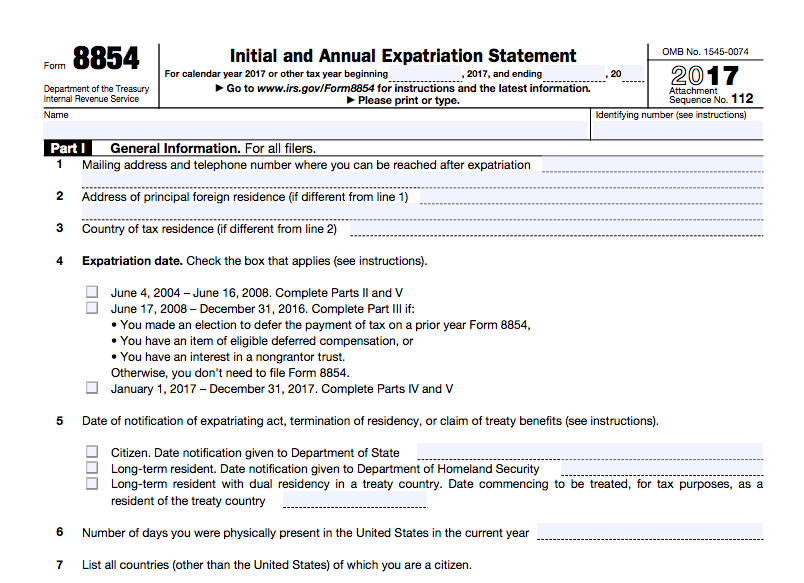

- You fail to certify on Form 8854 that you have complied with all U.S. federal tax obligations for the 5 years preceding the date of your expatriation or termination of residency.

As you can see, the only one of these factors you can control, is whether or not you file Form 8854. So everyone who’s subject to IRC. 877A needs to do that.

If one of the other triggers applies to you, then you’re a ‘covered expatriate’ no matter what.

And if you think one of the other two triggers could possibly apply to you, then you definitely need to talk to an expat tax professional who’s familiar with this provision.

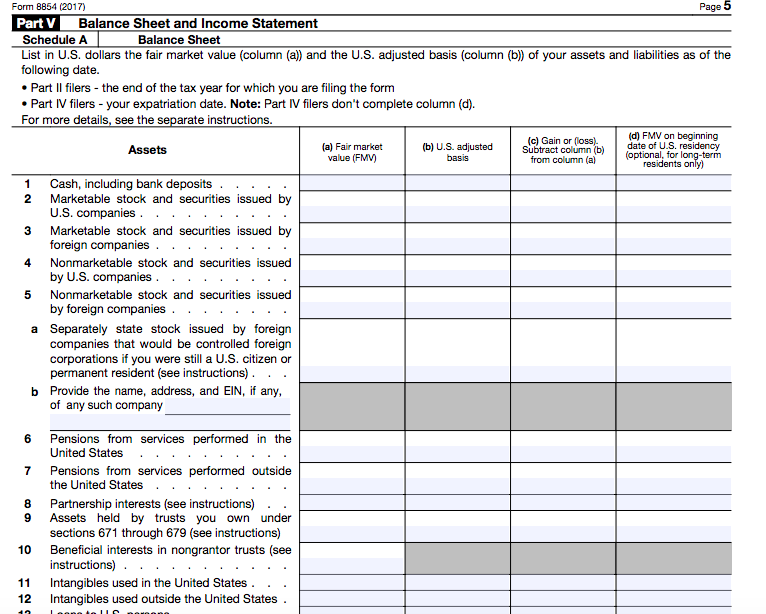

We won’t discuss the details of how net worth is calculated here, but that is probably the trickiest of the 3 triggers. Average net income tax for the past 5 years can be determined easily enough, by looking at your last 5 years’ tax returns (take line 63, ‘your total tax’):

So, to continue using myself as an example/guinea-pig, because I was a long-term Green Card holder when I renounced my Green Card, but because I didn’t quite have it like that to meet the net income tax or net worth triggers, I just filed form 8854 with my 2017 tax return, but didn’t owe any exit tax.

Venturing forward with at least an inkling of what kind of 877A requirements may apply to you, we can take the next step: actually filing the paperwork to renounce your Green Card.

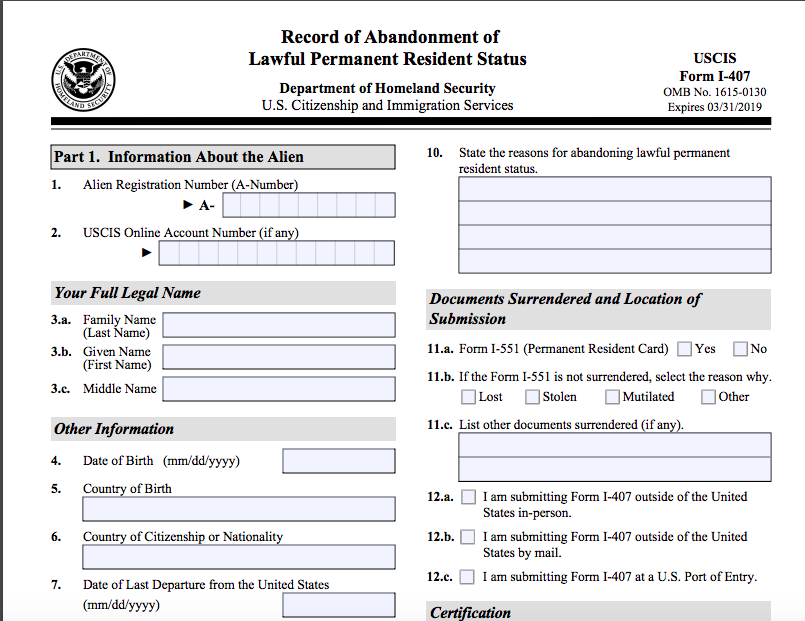

Step 3C: File form I-407

This step is entirely to do with your immigration status. The form you file is with the USCIS, not the IRS. But again, this is the step that ensures you’ll no longer be considered a US person for tax purposes, so it’s essential to make a clean break.

I’m not an immigration attorney, but from what I can tell, there aren’t any adverse effects of filing this form. It’s intended for you to proactively communicate your status to the US immigration authorities. Just letting your Green Card expire seems like the riskier choice to me, and it also has the negative tax results we discussed earlier.

So, for myself personally, I determined that filing for I-407 was the best course of action. I highly suggest speaking to an immigration attorney if you’re at all unclear on what the best course of action is for you.

If you’re going to file form I-407, you have two choices: in person, or by mail.

Filling out the form itself isn’t rocket science, but it can be tricky to figure out where to submit it.

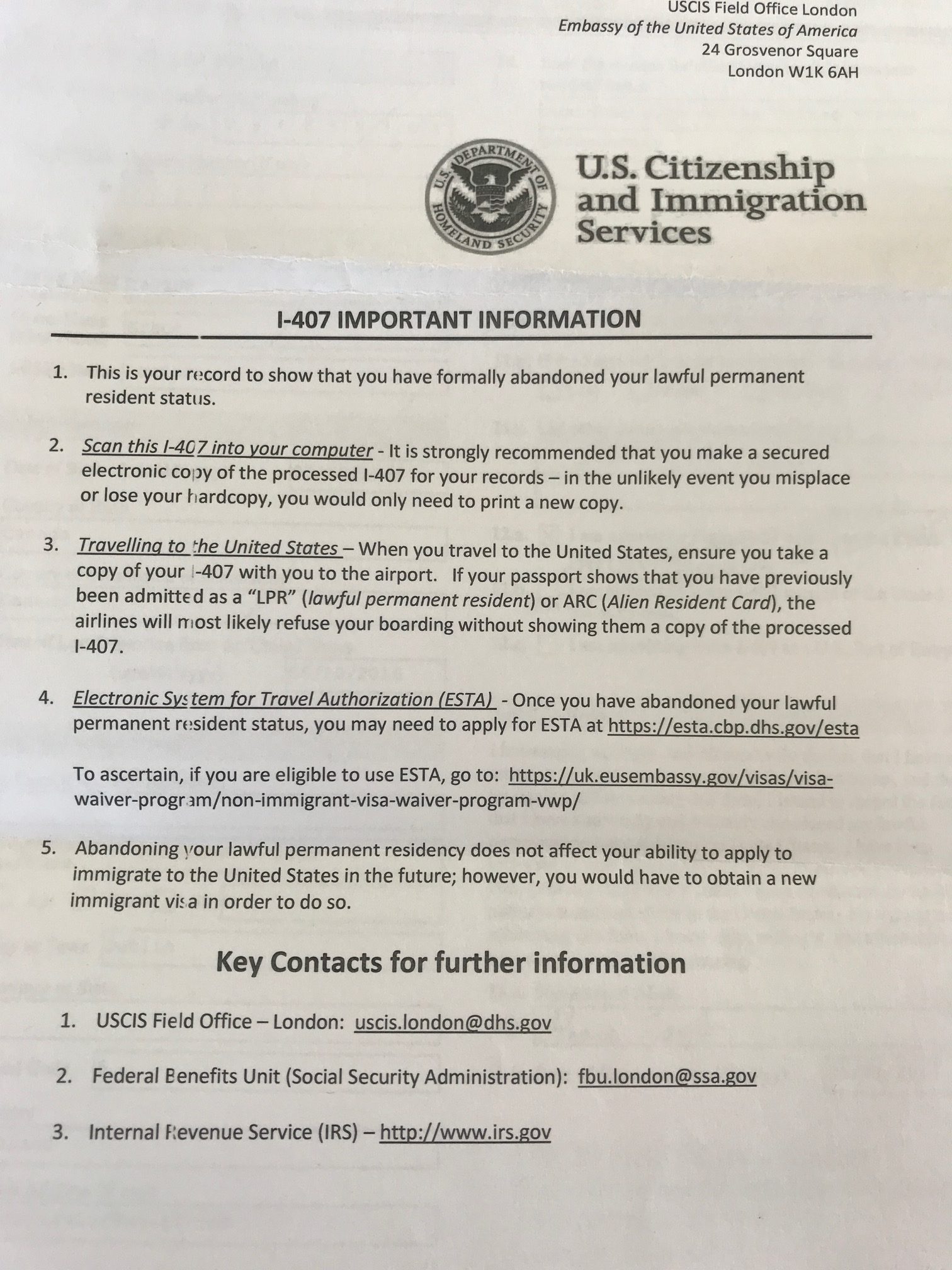

I first went into the US embassy in Dublin, as it appeared on their website that they could accept form I-407 in person. However, I was informed that they no longer do this, and I instead mailed my form to the London Field Office. You can look up a list of USCIS Field Offices here.

I mailed in my original Green Card, and I made a full copy of everything I had submitted, including the date I mailed it and the receipt of mailing. I would recommend doing the same, in case anything gets lost in the mail.

This is what I received in return, about 6 weeks after I submitted my forms:

I kept this, and brought it with me the first time I re-entered the US without my Green Card, but I wasn’t asked for it. I did state to the immigration officer that I’d previously been a Green Card holder but no longer held that status, and that was sufficient. I’d recommend bringing it with you the first few times you travel to the US without your Green Card, though!

Step 4: File your departure year tax return

So, you’re now officially a former Green Card holder, but you still have a very important task: filing your tax return for the year in which you gave up the Green Card.

This will be done in the same time frame as you’re used to: generally by April 15 of the following year, but the extension to Oct. 15 is still available to you if you need it.

As previously discussed, your departure year tax return will look different (dramatically so) from the ones you’d filed as a US resident. You really shouldn’t attempt to prepare it yourself; there are just too many moving parts, and you can’t use your prior years’ returns as templates because they’re totally different.

One additional variable on your departure year tax return, is whether or not you need to include Form 8854, under IRC. 877A. If you’re a long-term Green Card holder, you need to include Form 8854.

Your tax preparer will let you know exactly what information she needs from you for this. It will be helpful if you’ve recorded your personal ‘balance sheet’ as of your expatriation date.

Step 5: Future years’ tax returns, and other considerations

Now the heavy lifting is almost certainly behind you, in terms of your ongoing US tax obligations. You’ll be treated essentially like any other non-resident: you’ll have to file a US tax return if you have any US source income.

I’ll devote a future post to the specifics that non-residents need to be aware of, but usually you’ll know if you have US source income. If you have US investments, your US-source dividends definitely count. If you have a US rental property, that counts too. If you have business trips to the US, the income earned on those business trips should also be considered. So, depending on your personal circumstances, you may need assistance filing your subsequent non-resident returns as well.

This is especially true given the Trump Tax Reform that was passed in December 2017.

One of the facets of the sweeping tax reform, was the replacement of the personal exemption with an expanded standard deduction, ostensibly in the name of simplification. This ‘simplification’ complicates matters somewhat for non-residents, as we now know they’re not eligible for the standard deduction.

Previously, non-residents could typically claim a personal exemption for themselves (around $4,000 in 2017), and if their US source income was below that amount, they wouldn’t owe any US tax. They might not even have a filing requirement (although there are many, many scenarios where a tax return is required to be filed even if there is no tax due).

However, that’s no longer the case. Since non-residents can’t claim the standard deduction, and there’s no longer a separate personal exemption, the practical result of this aspect of the tax reform is to force all non-residents to file US tax returns when they have even $1 of taxable income.

Non-residents with small amounts of US source income should get used to filing, and paying, US tax, if their income doesn’t have US withholding at source. US-source dividends will often have US withholding at source, for example.

What other questions do you have? Anything you need to know about in further detail? Please feel free to let me know in the comments, or contact me to book a consultation if you need to discuss your personal situation.

Wishing you all the best on your globally mobile journeys!